In the high-octane world of Financial Independence, Retire Early (FIRE), the conversation is typically dominated by dividend yields, index fund allocations, and the "4% rule." For those sprinting toward a mid-life exit from the workforce, Social Security is often dismissed as a peripheral, "fuzzy" concept—a bureaucratic promise in the distant future that one shouldn’t bank on.

However, as the FIRE movement matures, its pioneers are discovering that Social Security is not merely a government safety net; it is a powerful, inflation-adjusted asset that can fundamentally alter one’s retirement math. By applying the financial principle of Net Present Value (NPV), we can transform this vague future benefit into a concrete tool for accelerating financial freedom.

The Paradigm Shift: Why Social Security Matters Now

For decades, early retirees have treated their personal "stash"—their 401(k)s, IRAs, and brokerage accounts—as the sole engine of their survival. The logic was sound: if you retire at 35, you need to survive three decades before you see a dime of government assistance.

But as the years pass and the retiree moves from their 30s into their 50s, the "distant" future begins to encroach upon the present. The realization dawns that Social Security is, in effect, a massive, inflation-indexed annuity. Whether you are 30 or 60, your future benefit represents a significant chunk of your total lifetime wealth. Ignoring it is akin to leaving a six-figure sum sitting on the table simply because you haven’t calculated its current value.

The Mathematics of Freedom: Net Present Value (NPV)

To integrate Social Security into your retirement strategy, you must stop looking at the monthly dollar amount you might receive in 20 years and start looking at its Net Present Value (NPV).

NPV is a financial metric used to calculate the current value of a future stream of payments. In simple terms, it asks: If I wanted to receive $X per month starting in 30 years, how much money would I need to invest today to reach that goal?

The Two Extremes

- The 30-Year-Old Retiree: For someone in their 30s, the NPV of Social Security is negligible. Because the time horizon is so long, the "discount rate" (the time value of money) effectively erodes the current value. You must still build your primary portfolio to carry you through the "gap years."

- The 60-Year-Old Retiree: For someone on the cusp of eligibility, the NPV is massive. If your projected benefit covers your cost of living, you are essentially "set for life." You no longer need to rely on the volatility of the stock market to fund your existence; the government has effectively provided you with a risk-free, cost-of-living-adjusted pension.

Chronology of a Retirement Strategy: The "Shane Survivor" Case Study

Consider the hypothetical case of "Shane," a 55-year-old who lost his savings in a business failure and fears he must work until 70 to survive. Conventional financial wisdom dictates that Shane should "tough it out" to maximize his benefit.

However, when we analyze the NPV of his potential payout, the math suggests a counterintuitive reality. If Shane retires at 62 and invests his payouts into a low-cost index fund, the compound growth of those early payments often outweighs the marginal gain of waiting until 67 or 70 to claim a higher monthly check.

By the time his more "patient" peers begin collecting their higher monthly payments at 67, the early retiree who invested their benefits has already built a "snowball" of capital that is mathematically difficult for the later claimant to catch up to.

Supporting Data: Why Working Longer Isn’t Always Better

The Social Security Administration calculates benefits based on your 35 highest-earning years. For early retirees, this often includes years of zeros. However, the system is progressive; it replaces a higher percentage of income for lower-lifetime earners.

The "Slacker" Incentive

A fascinating quirk of the Social Security formula is that it provides a "mild incentive for slacking." Because the benefit formula is weighted toward those with lower lifetime contributions, the difference in payout between someone who works 35 years and someone who works 10 years is often surprisingly small.

For example, simulations show that a person who works only 10 years might receive 45% of the benefit of a peer who worked the full 35 years, despite having contributed less than a third of the capital. This confirms that for the FIRE community, the "marginal utility" of working an extra decade to boost Social Security benefits is often lower than the utility of reclaiming that time for personal freedom.

Official Perspectives and Risk Mitigation

Critics of this strategy often raise two primary concerns: the potential for program insolvency and the argument that "you can’t live on Social Security alone."

The Insolvency Myth

While political rhetoric suggests Social Security is on the brink of collapse, the reality is more nuanced. Social Security is a cornerstone of the American social contract, with 73 million beneficiaries and a massive voting bloc. While benefit adjustments—such as means-testing for high earners—are possible, total cancellation is a political impossibility.

Furthermore, for the wealthy FIRE individual, a potential reduction in benefits is largely irrelevant. If you have built a sufficient nest egg, any Social Security payment becomes a "bonus" rather than a necessity. The risk is not a binary "all or nothing" threat, but rather a variable that can be hedged by maintaining a diversified, independent investment portfolio.

Living on the Benefit

Is it possible to live on the check alone? For many, the answer is yes. Data shows that millions of seniors live exclusively on Social Security, often by aligning their cost of living with their benefit. When an early retiree combines a paid-off home and a frugal lifestyle with a Social Security "floor," they achieve a level of financial security that is virtually immune to market crashes.

Implications for Your Retirement Timeline

If you are currently planning your exit from the workforce, your homework is clear:

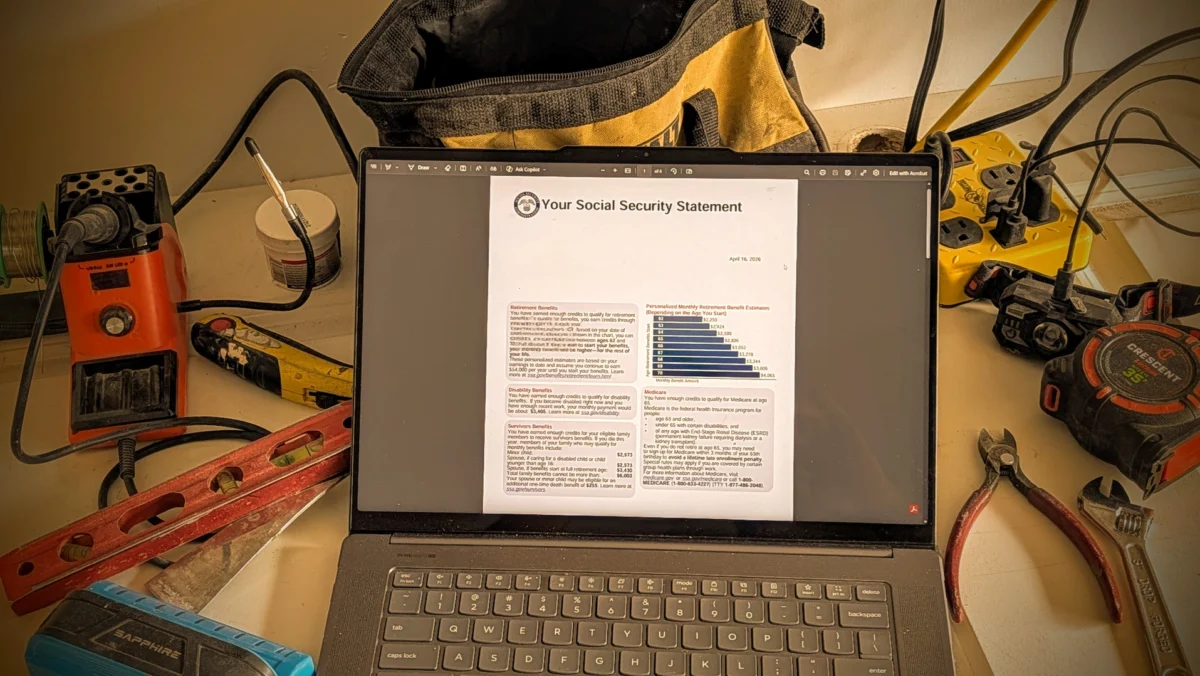

- Log in to SSA.gov: Create your account and pull your personalized earnings statement.

- Calculate the NPV: Use an online financial calculator or an AI tool (like Claude or ChatGPT) to determine the present value of your future benefits.

- Adjust Your Stash: Once you realize your future Social Security has a tangible value (e.g., $98,000 or $350,000 depending on your age), you can factor that into your "net worth" spreadsheet.

This is not a license to stop saving, but it is a license to stop worrying. Recognizing this hidden asset provides a "safety margin" that allows you to pull the trigger on retirement sooner than you previously thought possible.

Conclusion: The Path Forward

The fear of running out of money is the primary barrier to early retirement. By treating Social Security as a legitimate, quantifiable asset, we remove the "fear" element from the equation.

As we look toward the future, the integration of technology—specifically the use of AI tools to run complex, individualized NPV simulations—will become standard practice in financial planning. The goal is not to depend on the government, but to understand the tools at your disposal so you can optimize your life for freedom rather than mere accumulation.

The math is clear: you are closer to your "number" than you think. The only thing standing in your way is the hesitation to look at the data. Log in, do the math, and start planning for the life you want to live today, not in some distant, uncertain tomorrow.