While the global investment community remains fixated on the high-altitude, speculative euphoria surrounding SpaceX’s IPO, a more foundational, grounded, and arguably more critical transformation is taking place in the American housing sector. In a market dictated by the immutable laws of gravity—where supply chain bottlenecks, interest rate sensitivity, and land scarcity remain the primary drivers of value—Lennar Corporation has just delivered a second-quarter performance that serves as a pivotal stress test for the entire industry.

As the nation’s second-largest homebuilder, Lennar has long been the standard-bearer for the "asset-light" revolution. By shifting away from traditional land ownership toward a complex network of land-banking and option-based development, the company is attempting to rewrite the playbook for how a homebuilder survives and thrives in a volatile economy. The results from the second quarter suggest that, while the company has effectively silenced critics regarding its transparency, a much deeper, more consequential debate has begun: What is the true economic cost of operating a land-light model in a market that refuses to recover at the pace investors desire?

The Current Landscape: A Performance Summary

Objectively, Lennar’s Q2 results offer a compelling rebuttal to the skeptics who have questioned the firm’s structural stability. In an environment defined by the most challenging demand conditions since the post-GFC (Great Financial Crisis) era, Lennar not only met but in several key metrics exceeded analyst expectations.

The company reported adjusted earnings per share that surpassed consensus estimates, while gross margins landed comfortably within the projected guidance of 15.5% to 16.0%. Perhaps most importantly for institutional investors, the firm successfully navigated the "even-flow" production challenge—the ability to maintain consistent build schedules despite fluctuating consumer demand.

Lennar delivered 20,519 homes during the quarter and generated 21,749 net orders. While the order volume represents a slight 3.8% decline from the previous year’s second quarter, it falls squarely within the company’s internal projections. This is a remarkable feat of calibration, considering that these targets were set during a period of significant geopolitical and macroeconomic uncertainty. By proactively reducing speculative inventory, Lennar has demonstrated that its "asset-light" model is not merely a theoretical framework but an operational engine capable of real-time adjustments.

Chronology: From Scrutiny to Strategy

To understand where Lennar stands today, one must examine the evolution of the market’s narrative over the last four months. Earlier this year, the primary concern among analysts and institutional investors centered on the company’s complex web of land-bank relationships, specifically its ties to entities like Millrose. Critics argued that these relationships created a "shadow" leverage—hidden financial obligations and potential disclosure risks that were masked by the company’s accounting practices.

Lennar’s leadership team, led by Executive Chair Stuart Miller, met these concerns head-on. Through enhanced SEC disclosures, a detailed investor presentation, and exhaustive commentary during the second-quarter earnings call, management effectively dismantled the notion that these risks were opaque.

However, as the conversation shifted away from the "hidden debt" narrative, it migrated toward a more sophisticated critique. Analysts stopped asking if the information was disclosed and started asking if the model was sustainable. The transition in questioning—from "Are you hiding risks?" to "How do the long-term economics of this model function?"—marks a significant maturation in the investment community’s understanding of the modern homebuilding business.

Supporting Data: The Anatomy of the ‘Asset-Light’ Model

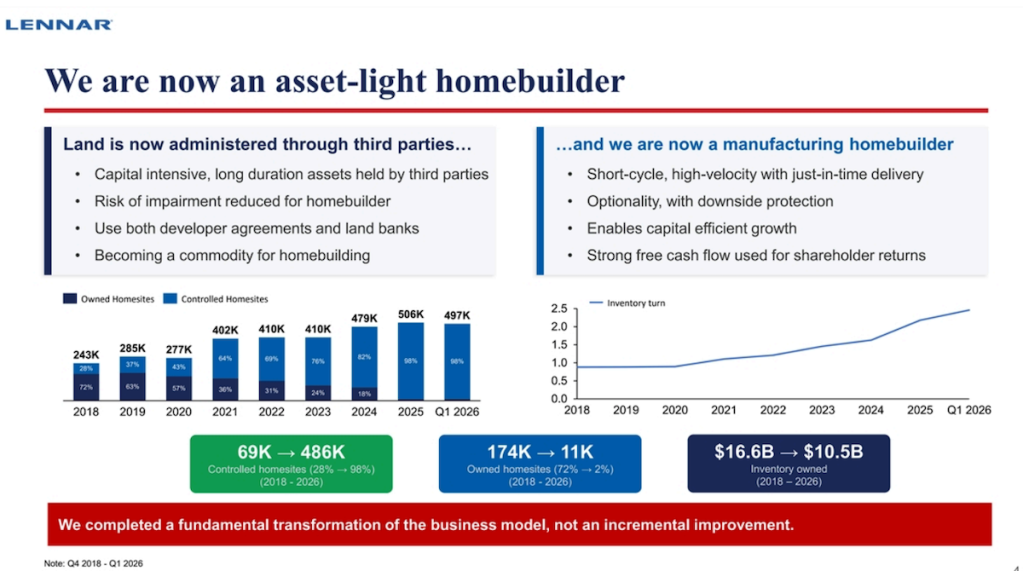

The shift away from land ownership is not a temporary defensive posture; it is a permanent architectural change to the company’s DNA. The data provided in the company’s latest investor deck is striking:

- Homesite Control: In 2018, Lennar owned approximately 174,000 homesites. Today, that number has plummeted to roughly 11,000.

- Controlled Positions: Conversely, the number of "controlled" homesites—lots accessed through options and partnerships—has surged to approximately 486,000.

- Asset-Light Concentration: Controlled lots now represent roughly 98% of the company’s total homesite position.

- Capital Efficiency: Lennar estimates that its current land-bank partnerships offload approximately $18.5 billion in capital requirements from its own balance sheet.

This data underscores the company’s pivot from being a "land investor that builds houses" to a "manufacturing platform that utilizes land as an input." In this framework, competitive advantage is no longer derived from land appreciation, but from purchasing leverage, production consistency, and capital allocation discipline.

Dan Oppenheim, a veteran investment research advisor, noted that the modest reduction in closing expectations for the year is actually a strategic positive. By not flooding the market with excess supply, Lennar is protecting its margins and maintaining a discipline that was historically absent in the boom-bust cycles of the past.

Official Responses and Strategic Reframing

During the earnings call, Stuart Miller was unequivocal in his defense of the strategic pivot. When pressed by UBS analyst John Lovallo regarding the timing mismatch between land-bank expenditures and future margin recognition, Miller framed the friction as a natural byproduct of a massive operational shift.

"What you’re seeing is the natural ebb and flow of capital," Miller explained. "As we transition from a land-intensive model to a manufacturing platform, there will be imbalances. These will ultimately equalize."

Miller’s rhetoric is consistent: Lennar is no longer defending a specific land-bank deal; it is defending a fundamental change in the definition of a homebuilder. He argues that the company should be judged not by near-term margin volatility, but by its long-term return on equity and its ability to remain resilient when market cycles turn downward.

Furthermore, Miller has begun to highlight the "policy wildcard." He noted that the level of federal attention directed toward housing affordability is "genuinely unprecedented." While he stopped short of providing actionable policy predictions, his conviction that government intervention is on the horizon suggests that Lennar is positioning itself to be a primary beneficiary of potential legislative or regulatory tailwinds.

Implications: The Industry-Wide Ripple Effect

The implications of Lennar’s success or failure extend far beyond its own boardroom. Because Lennar has pursued the asset-light strategy more aggressively and at a larger scale than any of its peers, it serves as the ultimate bellwether for the industry.

If the model holds, it will confirm that homebuilding has successfully transitioned into a modern, predictable manufacturing sector. However, if the economic costs of controlling land—through option fees, maintenance costs, and institutional capital premiums—continue to erode margins, the entire industry may face a reckoning.

1. The Margin Debate

The most significant unresolved question remains profitability. While a 15.6% gross margin is respectable, it remains far below the pandemic-era highs. The concern among analysts is that the costs of the land-light model are effectively "baked in" to the cost of goods sold, creating a new floor for margins that might be permanently lower than what investors historically enjoyed.

2. The Risk of "Hidden" Operational Costs

The debate has shifted from balance-sheet risk to income-statement pressure. Is the industry merely trading one risk for another? By offloading the risk of land ownership, have builders created a reliance on institutional capital that becomes prohibitively expensive during prolonged downturns?

3. The New Definition of Competitive Advantage

For decades, the "best" builder was the one with the best land positions. Under the new model, the "best" builder is the one with the most efficient logistics and the best trade relationships. This shift forces private builders and smaller competitors to decide whether to emulate this model or risk becoming obsolete in a world of high-efficiency, capital-disciplined giants.

Conclusion: A Test of Viability

Lennar has successfully proven that it can function without the heavy burden of land ownership. It has navigated the skepticism of the markets, cleared the hurdle of transparency, and established a robust, if complex, operating structure.

Yet, the final verdict is not in. The true test of this business model will not occur during periods of growth, but in the current environment of stagnation. As the industry grapples with stubborn mortgage rates and ongoing affordability constraints, Lennar’s performance will serve as the primary indicator of whether the "asset-light" strategy is a sustainable evolution or simply a sophisticated way to manage decline.

For now, the company remains the most important case study in modern residential development. Whether this model can generate the necessary returns to satisfy shareholders through a cycle of high interest rates remains the most critical, yet unanswered, question in the sector. Investors would do well to look past the headlines of the day and watch how Lennar continues to navigate this fundamental, and potentially permanent, transformation of the American homebuilding industry.